MRP glossary TOP > Cost Control > Cost Accounting

Cost Accounting

Cost Accounting

It refers to calculating the production cost in the manufacturing industry, and meaning a kind of procedure of adding the cost required for processing to the material cost.

Cost Accounting is performed for the following purposes:

Thus there are several kinds of Cost Accounting by purpose, and thinking of it from the standpoint of the category of industry/business the company belongs to, or of the standard for calculating costs and its range to be covered, Cost Accounting can be also classified into the following:

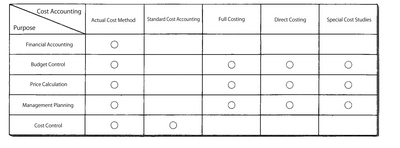

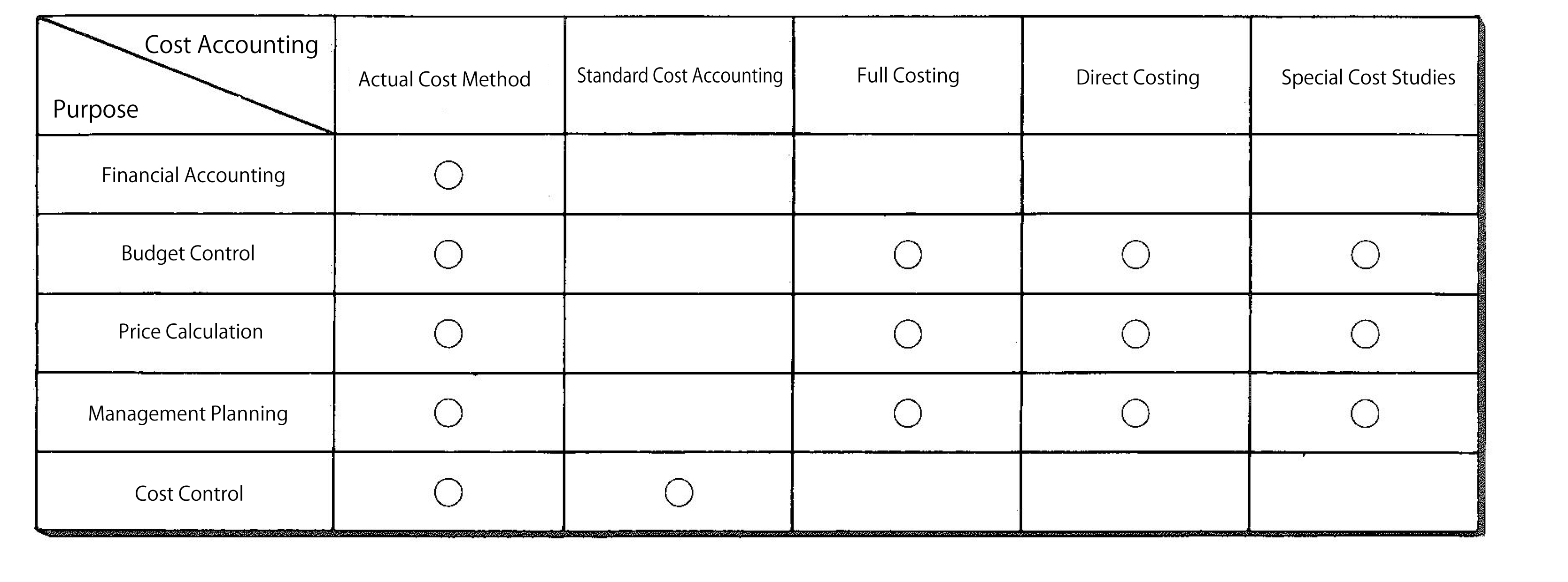

Looking at Cost Accounting by purpose, these various kinds of Cost Accounting are used as follows:

It refers to calculating the production cost in the manufacturing industry, and meaning a kind of procedure of adding the cost required for processing to the material cost.

Cost Accounting is performed for the following purposes:

- financial accounting:

- the documents for financial statements are prepared.

- budget control:

- the documents for budget drafting and control are prepared.

- price estimation:

- the documents for determining sales prices are prepared.

- management plan:

- the documents for profit planning and management planning are prepared.

- cost control:

- the documents for cost control are prepared.

Thus there are several kinds of Cost Accounting by purpose, and thinking of it from the standpoint of the category of industry/business the company belongs to, or of the standard for calculating costs and its range to be covered, Cost Accounting can be also classified into the following:

- the category of industry/business of the company:

- process costing and job costing

- the standard for calculating costs:

- actual cost accounting and standard cost accounting

- the range of costs to be covered:

- full cost accounting and direct cost accounting

- others:

- special cost studies

Looking at Cost Accounting by purpose, these various kinds of Cost Accounting are used as follows:

Reference:JIT Business Research Mr. Hirano Hiroyuki